A traditional group insurance model can be divided into two parts:

- Insured Benefits (life, LTD, AD&D, and travel)

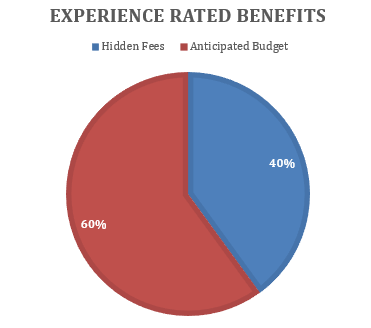

- Experience Rated Benefits (health, dental, etc.)

The bulk of your claims are made within the experience-rated benefits, in which lie hidden fees that are not shown on your renewal report.

Further, experience-rated benefits can be divided into two categories:

The 40% in hidden fees includes:

● Inflation: insurers add a certain percentage to mitigate inflation risk on the costs of medication etc.

● Profit: insurers need to make a pretty penny in exchange for their service

● Commission: the broker also needs his or her share of the pie

● Reserve: in the event that the client decides to leave the insurer, the insurer needs to ensure that they have surplus capital to pay out old and remaining claims

● Administration fees: the cost to pay out the claims, help employees and employers with the service

● SCAMQ: all companies in Quebec with a private insurance plan contribute to the Quebec Drug Insurance Pooling Corporation. This protects the client as well as the insurer from any major claims

● Stop loss: An extra layer of protection in addition to the SCAMQ, for major claims

Are all these fees necessary to maintain a healthy insurance plan? Absolutely not. In fact, the alternative group insurance model manifests that only administration, SCAMQ, and stop-loss are essential fees.